Introduction

It’s official, the world has changed and has done so at an alarming rate. Many retailers are finding this change difficult because of the pace at which it’s occurring.

Retailers around the world are seeking advice and guidance as to what the future consumer will look like, what changes are required to survive and grow in this new world which continues to evolve at pace.

The biggest issue at present is, all the published material being presented on a daily basis is fragmented and talks only about specific small pieces of a retail business. There is no published material which takes a holistic view and comprehensively looks at….

- Defining the new “COVID-Consumer” mindset?

- Explain why will COVID-19 influence permanent change in the consumer’s mindset?

- Define how must retailers plan and prepare to survive and thrive?

- Show what the key business activities need to look like in order for retailers to meet new “COVID-Consumer” expectations?

This research meets the above objectives.

The state of play:

Easing of restrictions:

As governments succumb to pressure, they will ease restrictions and allow people to go back to work and back into society prematurely. This easing will relax people and reduce the immediacy behind isolation and social distancing.

In many countries, this could result in new “waves” reactivating restrictions. This ebb and flow of quarantines and lockdowns will continue throughout the next 18 to 24 months minimum and won’t be completely halted until COVID-19 is proven to be under control.

Work and face-to-face social interactions will start and stop, making the home environment the only consistent in the world of the consumer for quite some time.

The Vaccine conundrum:

Politicians will be slow to communicate to the public the truth about a vaccine: will one be created, is it even necessary, or how long it will realistically take to be created and accessible.

Based on history, having no vaccine for COVID-19 is a realistic scenario.

Dr David Nabarro, Professor of Global Health, Imperial College London, and Special Envoy to the WHO for COVID-19….

"We can't make an absolute assumption that a vaccine will appear at all, or if it does appear, whether it will pass all the tests of efficacy and safety”

"It's absolutely essential that all societies everywhere get themselves into a position where they are able to defend against the coronavirus as a constant threat, and to be able to go about social life and economic activity with the virus in our midst."

While “Plan A” is for a vaccine to be produced, medical experts say, the world needs to develop a “Plan B”, a life where COVID-19 remains prevalent for years.

“Plan B” - life with COVID:

Medical experts have outlined specific characteristics as to what life with COVID this could/should look like:

- The culture of shrugging off cold symptoms and still going into work would be over.

- Remote working would become a standard way of life or at the very least, the days in the office should be limited.

- Companies rotate shifts so offices should never be unnecessarily full.

- Comprehensive programs of testing and contact tracing would be implemented. More than what is being seen at the moment.

- “Lockdowns” can and will occur from time to time when outbreaks occur. This will be more common during winter months.

This new “state of play” has considerable intrinsic impacts on the consumer, but will these permanently remain as part of the consumer’s value system?

What does the “COVID Consumer” look like?

How does this “state of play” influence a consumer’s information gathering, needs for engagement, buying motivations, and buying behaviours?

Consumers in the new world – defining the new “COVID Consumer”

While businesses are seen to be fighting to survive, the greater struggle occurring around the world is with people: their lives have been forcibly turned upside down. Everything a person defined as his/her own way of life has dramatically shifted against their own will.

To have this control pulled away has created widespread anxiety.

Concordia University applied specific research on the fear of losing control. Their results were published in Science Daily, which is summarized as…

People’s fears and beliefs about losing control puts them at risk of panic attacks, social phobia, OCD, post-traumatic stress disorder, general anxiety disorder and others

This is not to say every individual is succumbing to these conditions, but retailers need to gain this level of contextual empathy because it’s the above “state of play” combined with this loss of control in a person’s way of life that is contributing to the new “COVID Consumer”.

Why will the “COVID Consumer’s” mindset change be permanent?

A lot has been documented around how “permanent change is coming” but there are no clear explanations as to why it will be permanent.

For businesses, it’s important to answer the “why” question because business change must align to strategy. If a business cannot see the strategic merits in changing, it won’t happen and investment in a new direction becomes difficult to rationalise.

To answer the “why” question comes in two parts:

- The science behind behavioural change

- The differences between the 2008 GFC and COVID-19

The science of behavioural change:

Research from the European Journal of Social Psychology has proven it takes people 66 days of repetitive activity for new behaviours to become ingrained in his/her deeper “mental system” to become the new “way of doing things”.

A consumer’s “mental model” is the underlying “decision making engine” working behind the scenes to influence a consumer’s actions on all things. This behavioural system is developed from…

- The information a person gathers – access to information is now unlimited and dangerous

- Trying new ways to meet his/her needs

- Assessing the feedback once something new has been completed

If the feedback from trying something new is positive, it reinforces that behaviour, and stimulates a repeat of that new way of doing things.

It’s this repetition combined with continuous positive feedback which ingrains new behaviours.

The differences between the GFC and COVID-19:

Some businesses (retailers) have adopted the mindset, the world is going through something similar to the Global Financial Crisis (GFC) of 2008. While that singular event took years to recover from, businesses and consumer spending behaviours did recover and reverted back to how it was previous to that event.

Everything about this pandemic and how it’s affecting people and businesses is different. And as a result, the ripple effects will influence behaviour forever. To truly understand why this is the case requires analysis of the differences between these two events.

GFC = “balance sheet” recession:

The GFC was classified as a “balance sheet” recession that came as a result of inaccurate housing valuations. This resulted in a collapse in what economists call “the demand” which is consumer and business spending (tourism, retail, investments, trade, wholesale etc…).

COVID-19 affects supply chain:

While supply chains remained intact during the GFC, this has not been the case for COVID-19. COVID-19 has affected both supply chain and “demand” simultaneously. Productivity across the globe was forcibly shut down

Added to this, COVID-19 has delivered a new global fear of the vulnerability to supply chains both now and in the future. Compounding this fear is the degraded confidence in China, a fundamental supply chain source for a significant part of the world.

China is the single biggest exporter with total exports in 2019 totalling $4.4 trillion (US dollars).

Physical retail remained open during the GFC:

Though retail was affected by the GFC, physical retail stores remained open and could effectively adjust to the times by immediately working with frontline staff to change policies, procedures and pricing strategies to cope.

In 2020, retail stores were closed (now gradually reopening) forcing retailers to change via the technologies and business systems they depend on. Those retailers who did not adequately invest in technology prior to shutdowns have been exposed in the form of exhibiting poor online retail experiences.

The reliance on technology for retailers back in 2008 is nothing like it is today.

GFC had a known cause and cure:

The communications from government on how to recover from the GFC was clearer because they understood the cause. The GFC was referred to as a “subprime” virus which had an “economic vaccine”. Even though there was a slow recovery, a plan was clear.

COVID-19 has brought global uncertainty in…

- It’s origin

- Effective and efficient testing procedures

- The proper method to treat once people have the virus

- If/when a vaccine will be available

Financial markets historically perform poorly under uncertainty.

Access to information is unlimited:

Due to consumers having a super computer in the palm of their hands (smartphone), every individual literally has unlimited access to information. Whereas in 2008, the first smartphone was just being released.

This increase in transparency on what is occurring (and not occurring) around the world and locally, is amplifying anxiety. Where in the past if governing bodies dealt with a crisis and had little clue how to resolve, this was not nearly as obvious as it is today.

COVID-19 is killing people:

Though the GFC did influence suicides, this was not well publicized. COVID-19’s known effect on human life is a continuous dominant message in the media.

GFC did not affect everyone:

Though the GFC was a big event, it did not affect everyone globally. COVID-19 has.

For retailers who think they can “wait this out” as if it was like the GFC, the message here is….don’t.

Consumer Research – the new methodology:

Due to the pace of change, international research organisations have adjusted their method in research and analysis of the new consumer behaviours.

The top firms have been working overtime in the last 14 plus weeks to assist in uncovering what these new consumer belief systems look like and have undertaken a unique methodology where “waves” of survey research is being applied.

This is the process of surveying large volumes of consumers around the world asking specific questions, and then going back to these same groups with the same questions at weekly intervals to see if there is accurate trending in the responses. Combined with this is the introduction of new control groups each week to determine if responses are similar.

This is to ensure these control groups are represent the wider market sentiment.

When a response dramatically changes from one week to the next, it is deemed unreliable and not used.

The research below looks at consumer behavioural trends that have been verified by this “wave” methodology. All of the research relates to consumer behaviours in the context of how they feel about retailers, and how they wish to engage and purchase.

The COVID-Consumer Trends:

Trend: Consumers expect to reduce their out-of-home leisure behaviors

2 in 3 consumers say they expect to reduce how frequently they engage with various out-of-home leisure activities.

Restaurants are top of the list for a reduction; over 40% anticipate they will eat out at restaurants less frequently. More reluctance comes in the form of eating at fast food outlets and visiting bars, pubs and movie cinemas.

Over 40% say they plan to exercise at home more frequently after the outbreak, and 1 in 10 say they expect to cancel their gym membership.

Another “out of home” leisure activity not high on the priority list is the “live events industry” which is comprised of the following…

- Sports stadiums

- Music festivals

- Concert halls and Theatres

SAP conducted research specifically on this type of activity and found 80% responded by saying they are not comfortable attending a live event. Though the passion and love for such things as professional sports remains high, the desire to view an event amongst crowds is not deemed favourable.

Trend: Discovering and seeking out new connections and nurturing relationships remotely

Youtube is playing a big part with videos where the demand for titles such as “cook with me” or “workout with me” continue to grow.

People are also looking for new ways to connect with people from afar. Search interest for multiplayer video games has spiked globally in the past few months.

Search interest for “virtual drinks” in Australia and New Zealand is highest worldwide.

Trend: Consumer acceptance of less privacy

The 9/11 event prompted the societal acceptance of increased community surveillance. This (apparently) was the key to keeping people safe from future terror attacks.

This opened up a wider acceptance for the likes of Facebook to learn more about an individual in exchange to access to messaging APP’s and more relevant content.

COVID-19 is taking this to another level with the presentation of APPs which monitor a person’s every movement in the effort to improve contact tracing. Governments are using freedom as leverage for this data and is aggressive in its messaging to prompt consumers to download an APP.

Technology is being hailed the savior to provide the transparency needed to control the spread of COVID-19.

Whether a consumer likes it or not, the message here is, governing bodies are leveraging freedom with a consumer’s privacy, and as a result, having less privacy will become the new normal.

Trend: Empathy is growing

The “COVID Consumer” is becoming more in tune with the suffering of others AND the well-being of the planet.

The benefits of the planet and the reduction in pollution has been openly documented with stories and imagery showing how polluted areas are clearing as a result of manufacturing, logistics, and airlines having ceased working.

Empathy for people is reflected in the increase in search behaviour for certain terms and phrases such as “how to help” and “alone together”, increasing dramatically.

Consumers are being seen to be looking for ways to give back and help the vulnerable in their communities.

This empathic view has created a reprioritization of the who, how, when, where, and why of consumption and forcing a “rethink”.

Though the consumer does not expect organisations to change, those who do, will benefit.

Retailers who seek to improve the perception of their brand have an opportunity to tap into this new expectation. Consumers think favourably of brands who…

1. Show support during the COVID-19 crisis in some way: donations, creating equipment, working on the planet.

2. Are seen to assist regional governments: 89% of Americans believe the government alone cannot stop the spread of coronavirus and need help.

3. Retailers who help consumers in some way such as

- Providing advice on how to improve their own life

- Providing reliable information because the media is in contradiction

- Advising how to be healthy at home

- Offering tips on how to relax and reduce anxiety

Those brands who demonstrate how they contributed to “good” will find it easier and faster to bounce back compared to those who merely focused efforts on contacting consumers with campaign driven content.

“Brands that can show they are putting people or the environment ahead of sheer profit will be rewarded by consumers and employees and enhance the way they consider the brand.”

George Wallace, chief executive, MHE Retail

Trend: Anti-excess consumerism

The extension to the growth in empathy from consumers is redefining their perception of “excess”. Where excess was once seen as a “badge of honor” the pandemic has reshaped the consumer’s thinking on non-essential spending.

The same behaviours was seen during the GFC, with the only difference being, luxury brands had all their physical retail stores open to assist in the recovery.

For luxury brands, the “physical store experience” plays a key part in the buying journeys of many consumers. This combination of a consumer’s rethink and store closures will affect this industry.

Research has seen an immediate shift in support for brands exhibiting behaviours around anti-excess and recycling.

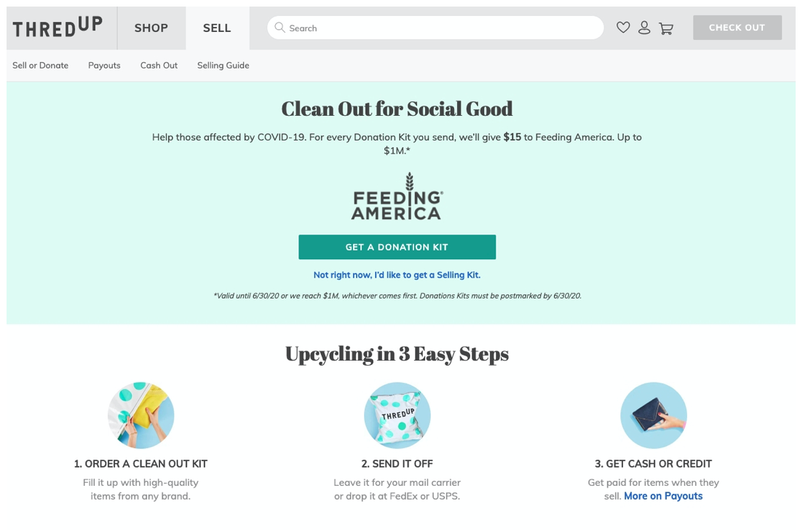

One example of this in action was seen in April 2020 where Abercrombie & Fitch and Reebok partnered with clothing resale website ThredUp. Customers can sell unwanted high-quality clothing to ThredUp and earn Reebok loyalty points or Abercrombie gift certificates.

Figure 1

Trend: Aware and concerned with Supply Chain

Though supply chain is a known business issue, it has significant ripple effects to consumers, resulting in a change in behaviours.

The “COVID Consumer” is seen to be gravitating back to more known brand names when purchasing online.

There is the perception known brands have a more solid, established, and reliable supply chain.

This is a complete flip from pre COVID times where consumers had less loyalty for brands and would engage with retailers who appears to better meet his/her need.

Consumers still demand great end-to-end experiences; however, reliable delivery promises now to rank much higher than before.

The “Reliable Delivery” promise:

Research has proven, the “reliable delivery” offer is now ranked as high as free delivery offers in terms of perceived value by the “COVID Consumer”. KPMG Australia supports this statement by saying...

While the leading brands list in 2018 and 2019 was dominated by airlines and financial services, our research conducted at the height of Australia’s lockdown saw consumers shift towards safety, security, transparency and reliable delivery.

This has come as result of the logistical chaos consumers have been exposed to when buying online and experiencing the following….

- Retailers have “over-sold” and must credit back purchase amount

- Delivery to home is taking significantly longer

- Calls to retailers to find out the status of the delivery is met with no certainty

- No confidence in click and collect experiences being safe

If retailers can guarantee order delivery to specific timelines, they will win customers.

Amazon’s “COVID-free” Supply Chain:

Amazon has recently promised to invest $4 billion into COVID-19 specific initiatives.

There is a long list of ways Amazon will be investing in the pandemic however one of the most notable investments will be in the creation of a “near-virus-free supply chain”.

Amazon will work to ensure a high standard of reliability will come from this retailer as a result of them creating a supply chain environment that will be either free or “near COVID-19 free”.

Amazon is confident they can achieve this because of the strides they are making in owning the “last mile” logistics.

As recently as February 2020, terminated another three delivery contracts from large logistics companies in Washington state and Texas.

Walmart cannot compete.

Figure 2

To offer “COVID free” delivery is something that will resonate with consumers.

This investment and the lengths Amazon is undertaking offers proof, one of the largest retailers in the world knows the future will forever change as a result of COVID-19, and they are adopting a “Plan B” way of business life.

This should be a signal to every other retailer in the world to prepare for the new “COVID Consumer”.

Trend: Return to bricks and mortar will be slow

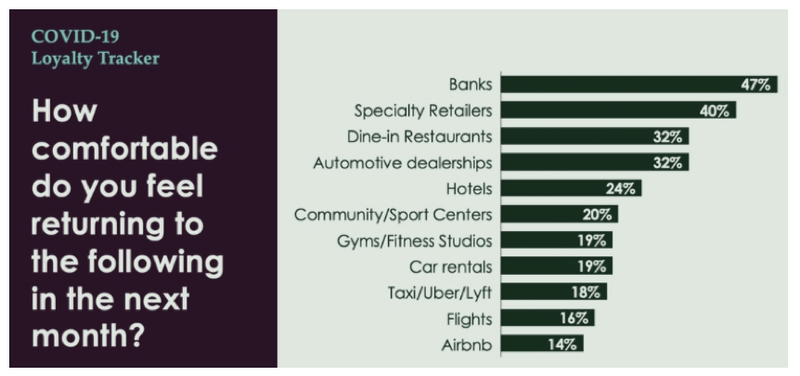

Over half of global consumers say they will not return to shops for “some time” or “a long time” after lockdowns ease.

9% of shoppers say they will return to stores “immediately” once restrictions ease.

This predicted behaviour of consumers raises concerns over how quickly brick-and-mortar stores, and the retail industry in general, will bounce back post COVID-19.

Figure 3 shows the consumer’s view as to the extent to which they feel comfortable in heading back to an array of different business and industry types.

Though Banks appear to be the highest in how comfortable consumers feel in returning, this data shows that less than half (47%) are prepared to go back. This is how the data should be interpreted for each industry and business type seen in Figure 3.

While “specialty retailers” appears to be high on the list, this is a retail business where the products are unique in nature, different from a department store for example.

Figure 3

The final “wave” of data in Figure 3 was completed in April 2020.

Of high importance to retailers, other research identified for those consumers who eventually head back to engage in physical bricks and mortar locations, they intend on spending less time in store.

This is significant to for retailers to acknowledge. This insight becomes crucial later on.

The research suggests there will be an initial surge in physical retail shopping once restrictions ease, but this will be short lived. This will be due to a knee-jerk reflex of being locked away at home for an extended period of time.

Slow return to retail in China:

In China, physical retail has quickly reopened. Despite the removal of formal lockdown orders and stores reopening, the pain for traditional retailers has not yet abated.

77% of retailers saw foot traffic sitting just above 50% of pre-COVID levels.

Trend: Consumers waiting for promotions

Almost 1 in 3 consumers say they will wait for products to be on promotion. They are also four times more likely to hold out for promotions for a trusted brand rather than looking for cheaper options from an alternative brand. This supports statements made earlier about supply chain reliability.

Consumers looking for luxury items feel the same way. They will wait for a promotion than take any of the other actions, suggesting an opportunity to galvanize loyalty and encourage spending through the use of offers.

Trend: Consumers gravitate to “local” retailers

There is a strong lift in interest in engaging with “local” businesses.

This need to engage “locally” comes in two contexts…

- Engaging with retailers nearby (proximity), and

- Engaging with a retailer who sources products and services locally

Engaging with retailers nearby:

Being confined to your home makes proximity a bigger consideration when deciding on who to engage within retail.

This hyper-focus on local is also an extension of the growth seen in empathy, where there is a growing desire to keep the money in the local community.

This is a natural human instinct of survival and a sense of belonging. Social psychologists state the intrinsic motivation to need to belong to a community during a pandemic has come as a result of social distancing, cancelled gatherings, working remotely, travel being eliminated.

Look no further than the “neighborhood street gatherings” to see this in action. This sense of belonging and need to support the local community extends out to retailers.

Sourcing Local:

The sourcing local need has come off the back of the global tensions with China which is not going away anytime soon.

Nielsen’s has found consumers are steering away from products that travel long distances, requiring multiple human touch points. This is a mix of product categories and foodstuffs, illustrating the significance behind Amazon’s new approach in creating a “COVID-free” supply chain.

Trend: Online shopping will continue to grow:

The “multibillion-dollar” question all retailers want to be answered is…

Will the significant lift in online purchasing behaviour being seen at present, remain post-COVID?

The short answer is “Yes it will”.

Some proof points….

Over 40% say they will shop online more frequently after the outbreak. Figure 4 represents those who “strongly agreed” or “somewhat agreed” to the question of “will you shop more frequently online”. What is of high interest is, as the “research waves” continued, the “yes” responses grew overtime.

This upward trending reflects the science of human behavioural change mentioned earlier: as the feedback continues to remain positive, the new way of doing things becomes more embedded. As consumers continued to shop online and have good experiences when they were asked again if they would continue, more responded with “yes”.

Figure 4

Retail trending data shows in April 2020, traditional retail businesses (defined as those who have a large physical footprint) saw the number of “first time” purchases being conducted online grow by 119% when compared to April 2019.

There has also been a significant return to shopping APPs. The number of APP “reattributions” (a consumer has returned to an APP) increased by 43% in April 2020.

The Caveat:

While the data and trends look positive for online buying behaviours of the “COVID Consumer”, there is a caveat…

Retailers must work harder to enhance and create amazing end-to-end online buying experiences

While online buying is becoming more embedded into the new way of doing things a consumer’s tolerance for poor experiences has not changed. In fact, this tolerance has become lower due to the high occurrence of bad experiences being experienced by retailers who have been caught unprepared.

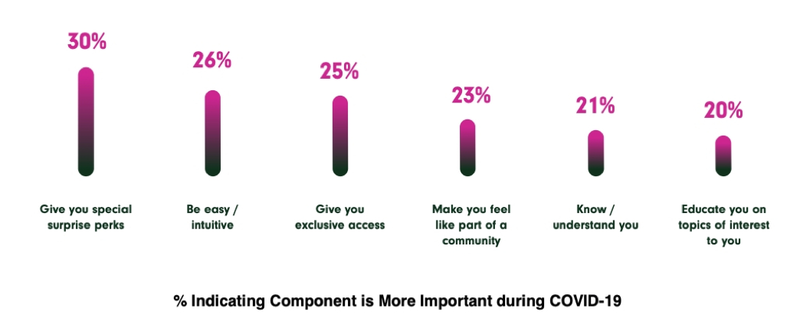

Figure 5 (below) is the result of research asking people what’s important to them when engaging with retailers online during COVID-19.

Of the top six responses, four relate to delivering great experiences….

- “Be easy/intuitive”

- “Know/understand you” (translation: be relevant)

- “Educate you on topics of interest” (translation: be relevant)

- “Give exclusive access” (translation: make me feel special)

Figure 5

The “COVID Consumer” is sending clear signals to retailers around the world. They want to engage and buy digitally and will continue to do so if new needs and expectations can be met.

The focus now turns to the conduct of retailers on what they must do to plan for change and set a course for evolution to keep up.

Managing business crisis in unprecedented times

The new belief systems, anxieties and outlooks on life seen in the previous section has resulted in businesses to move into a mode of crisis for four reasons…

- The pace at which the “COVID Consumer” evolution is occurring

- Businesses are not designed to evolve and change this rapidly

- Businesses are struggling to find the right direction in which to change

- The majority of businesses are operating on low cash reserves

Half of UK retailers could be wiped out if coronavirus continues. Modelling by Retail Economics shows a 10% reduction in sales would result in over two-thirds of major UK retailers to fall into negative cash flow: sales shown to have dropped as much as 70% since March 2020.

In April 2020, Debenhams appointed administrators in the hope that it will be able to salvage as many of its UK stores as possible.

All retailers are operating in crisis, but most notably are those with bricks and mortar footprints.

Even though what retailers are facing today is unprecedented, history has proven, when businesses effectively manage themselves in crisis, they set themselves up for long term growth.

The challenge retailers face is how to manage this crisis and at the same time pivot to leverage the opportunity coming from the online channel.

Crisis management 101:

Managing crisis can be summarized in three steps…

- Executive team takes responsibility and leads

- Listen to customers and acknowledge issues

- Apply rapid change

(Source: NYU Stern School of Business)

Step 1 – Leaders take responsibility:

The realization of being in crisis requires a paradigm shift within the executive team. Only once this occurs can the business then activate a crisis plan.

The executive team holds the strategic vision, they control the purse-strings and steer business resources. Only once this team is unified can it move on to step 2 of listening to customers and acknowledging issues.

Step 2 – Listen to customers and acknowledge the issues:

The act of identifying and acknowledging issues comes in three forms:

- Identifying the change in customer behaviour and understanding what their new motivations and needs look like

- Identify the new gaps between the current business offering and this new customer expectation shift

- Acknowledging the anxiety felt by staff during this chaotic time

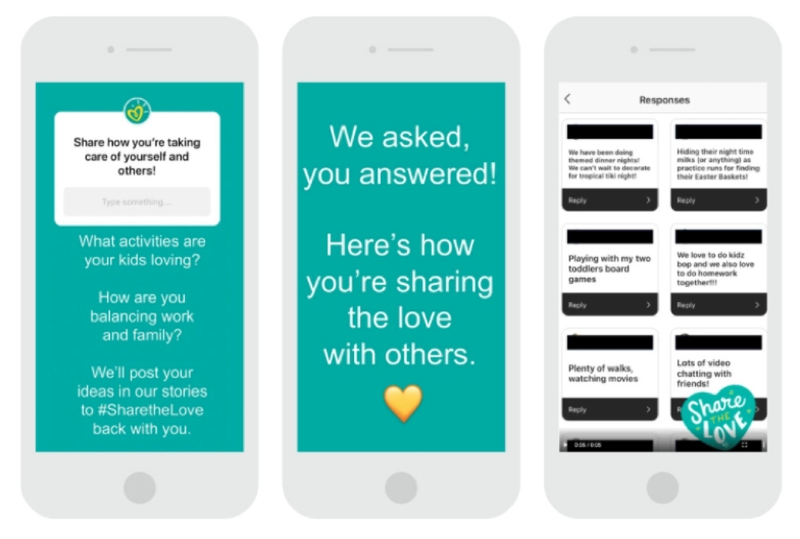

There are many ways to listen. Analysing behavioural and qualitative data sets form the foundation to develop the right insights, but there is also the act of simply asking your customers. The “COVID Consumer” is more open to sharing personal information now more than ever.

Pampers did this by asking their “fans” what they are doing during lockdown. Pampers then responsibly shared this via their site and social but internally used this data to assist in decision making.

Figure 6

This drove engagement both with fans and helped the brand understand new needs and expectations.

Why is listening to the “COVID Customer” important?

The most common side effect of a business in crisis is it becomes internally focused. The business is fighting and struggling to survive and looks within to find the answers. They focus on…

- Employee layoffs

- Seeking government support

- Cutting costs

This internalized approach is the exact opposite to what is required for a business to survive and thrive during “COVID times”.

Retailers who become more “empathetically in tune” with their customer will be better prepared and equipped to adapt in the right direction.

Step 3 – Apply change rapidly:

WHO recently released a statement meant for nations, but it applies to businesses in crisis…

“If you need to be right before you move, you’ll never win. Perfection is the enemy of the good when it comes to crisis management. Speed trumps perfection.”

(Source: WHO)

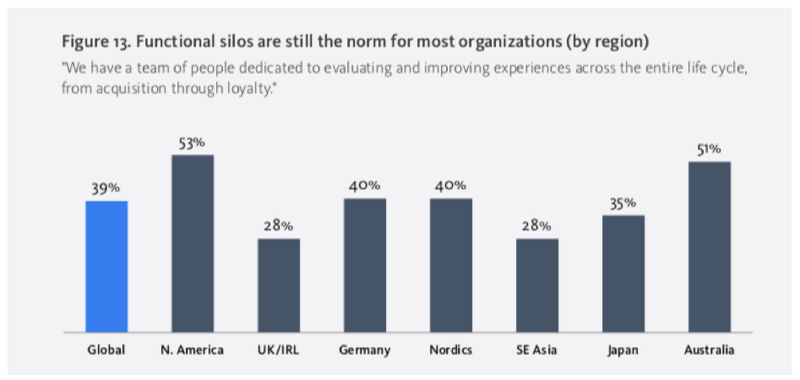

“Organizational agility” is a new characteristic all must adjust and adhere too. Agility is problematic for older organisations who are bureaucratic in nature, has multiple management layers and departmental silos.

Figure 7 below shows the global average of businesses who are designed to support customer experiences elegantly across departments is 39%.

Figure 7

Rapid execution comes in three steps…

- Strategic prioritization – the data driven process drives priorities

- Execution through collaboration – specialists need to work together to bring change

- Heighten listening skills – use data to define if the change is adding value

Why are retailers struggling to change?

It’s easy to sit back and watch the experiences degrade as online channels become busier, but it's important to understand why many retailers are struggling. To define the reasons as to why some are failing helps others in their decision making on how to design (or redesign) their business to move forward.

The answer to this comes down to how businesses have been originally designed in “Pre COVID” times which can be summarized in two steps…

- Systems were first established and would dictate what information is captured and how it needs to be processed. Think of the outdated ERP systems currently in play.

- Processes then reflect the needs of the systems and in turn dictates the conduct of employees and how they treat and serve customers.

Together, systems and processes become the primary influencer of customer experiences.

Overtime, systems and processes change when something “bad” happens to the business. This change is to prevent a recurrence to protect the business with little thought of the consequences being made to the customer experience.

Employees then become constrained and have little flexibility. The poorly designed systems and processes of a business then becomes the consumer’s problem.

This is what we are seeing today. Rapid consumer change combined with poorly engineered businesses resulting in a myriad of poor experiences.

This entire method of engineering business needs to be flipped on its head:

- A process of listening to the customer should define how a business is to treat them

- This listening brings clarity and defines employee conduct and supporting processes

- Employee conduct and processes then influence system design, information transfer and information gathering

This is what is meant when a business is “customer lead”. The customer leads the design of the business. This is how retailers need to approach change in order to keep up with the “COVID Consumer”.

Any attempts to keep up when systems are designed first, leads to failure.

The “Retailer” New Reality

This is what we now know….

- The impacts of COVID-19 will be long lasting and will permanently influence consumer behaviorisms and their own internalized belief systems forcing a rethink in how the engage and buy with retailers

- There are many new characteristics of the “COVID Consumer” that retailers must now be cognizant of

- To work through business crisis, retailers must listen to the “COVID Consumer” first, followed by the creation of processes and systems

- This all must occur at pace

The new retail mindset:

Put simply, COVID-19 has flipped retail on its head. Before the pandemic, digital retail was growing but it still complemented the physical retail experience. This is no longer the case.

Physical retail is now a complement to the digital retail buying experience.

Once retailers change their mindset to recognise this new reality, they can then prepare themselves for the future.

To assist retailers in their evolution, there is research coming out highlighting specific business characteristics that are seen to be significant factors in a retailer’s ability to survive during these tough times and prepare them for growth long term.

There are success stories being seen where retailers are performing at 60% to 80% of total retail sales coming solely through their online channel, while their physical bricks and mortar remain closed.

The research now turns to identify the characteristics of these retail models and what they are doing very well to activate this type of business performance. This section summarises those characteristics found across multiple retail businesses.

#1. Employees:

The rapid evolution of a business does not happen by robots, AI, or algorithms. It’s people.

Certain businesses recognise the importance of employees and the role they play in working through crisis. While a business is holistically focused on production and outcomes while in crisis, it needs to understand where this comes from….it’s people.

Technologies are valuable but they are driven by people no matter how sophisticated it may be.

Some examples of what these retailers are doing…

- Introducing remote working options, this includes introducing and investing in technology that assists in improving connectivity between remote teams.

- Show trust by “loosening up”. Allow flexibility in work hours when employees are working remotely.

- Improving office settings so employees feel safe.

- Changing/enhancing sick leave options during the pandemic. Where many used to feel taking sick leave was a taboo, it should now be welcomed and supported.

- Be transparent and vocal. Send regular updates on the company and what it’s doing during high degrees of change.

- Show gratitude by giving recognition to employees to drive a sense of belonging and positivity.

Some examples of what Amazon has recently done….

- Offering unlimited paid sick leave for those who test positive for COVID-19.

- Setting up “COVID testing stations” in their warehouses around the US (making employees feel safe).

- Provided a raise to all warehouse employees (showing gratitude).

If employees do not feel good about the company they work for and the environment in which they work in, there is no way they can handle the change that is occurring and to service and treat customers to a high standard.

#2. Service Design

Service design is the act of a retailer injecting employees throughout a consumer’s buying journey to ensure there are human touch points across his/her entire experience.

With the dramatic increases seen in the engagement of the digital channel, injecting the “human element” into online shopping is more important now than ever before.

The Service Design function and how it works digitally is broken down into three sub groups…

- Sales

- Support

- Recovery

Sales:

The sales subset is a proactive sales focused approach. These are essentially sales people who are readily available to engage with consumers online who have questions or need guidance on their purchase decisions.

These people are the product subject matter experts, stylists and build confidence a consumer’s buying decision making. Data proves when consumers engage with these employees, they convert online anywhere between 15% to 25%.

This method of engagement is typically achieved via incoming phone calls, social or live chat.

Support:

The dynamic behind the support function has changed for businesses and the “COVID Consumer”…

- Consumers are dealing with situations they have never faced before

- As a result, support teams are dealing with questions they have never dealt with previously

- The volume and frequency of requests have increased since the shutdown periods began in March 2020

The Harvard Business Review (HBR) conducted a study where they researched over 1 million incoming customer service calls from mid March 2020 to mid April 2020.

They ranked the calls from “easy” (standard questions easy to resolve) to “difficult” (unique requests/questions that are complex and difficult to resolve).

“Difficult” calls are complex because they reside outside of standard business policies and procedures.

During this time, the HBR found those calls labelled “difficult” had more than doubled.

Furthermore, the data also proved, that when “difficult” calls were not properly resolved, there was over a 90% likelihood, the business was going to lose that customer.

“High effort (difficult) interactions with customers are far more likely to lead to churn and far less likely to result in any sort of new sale”

Remember the discussion earlier about how business systems and procedures are set without the customer in mind. This is an example of the ripple effect brought on by this type of business design.

Those retailers seen to be delivering great customer support to the “COVID Consumer” have two similar characteristics…

#1. Empower employees to resolve the issue:

Even if it requires an employee to work outside of standard policy and procedure, if the mandate is to make the customer happy, they make it happen.

Those support employees who “hide behind policy” and state they are “powerless to help” are seen to be failing.

#2. Enable collaboration:

The act of collaboration and sharing “customer stories” with colleagues is working.

Support teams have two fundamental issues…

- They don’t know what calls are coming their way, and

- They don’t know how to resolve “difficult” calls

Through collaboration, one member can share a “difficult” call and how they resolved it, equipping and preparing others.

#3. Informing executive:

The “difficult” calls are logged and reported to management to show business decision makers what queries are coming into the business residing outside of policy.

This is a valuable form of “listening” and is strategic…

Though change is driven from the top down, executive decision-making should be influenced by the bottom up.

Recovery:

When a retailer “recovers”, it is an employee (or group of employees) who work outside of existing business systems and policies to meet the customer’s expectation. Due to the growth in “difficult” enquiries, this is seen as an important extension to the customer support function.

Figure 8

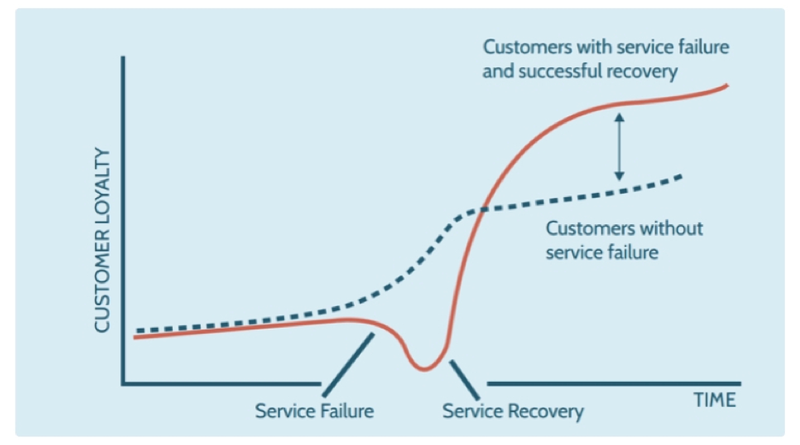

The power of recovering has many benefits with one being an increase in customer loyalty. This is known as the “Recovery Paradox”: see Figure 9 below.

Figure 9

A customer responds favourably when they perceive a business is bending rules to make them happy. However, if a customer thinks this error will repeat, the effort of recovering will not work.

“When customers experience a service failure, they ask themselves whether the failure has temporary or permanent causes, and if they think that the problem is likely to occur again, they will avoid this business in the future.”

This is why a business should activate two steps when empowering employees to recover…

- Resolve the issue

- Report the issues and the necessary solution to the executive team to drive change

According to Gartner, only 4% of retailers are conducting a support and recovery function to a high standard signalling a clear opportunity.

#3. Streamline and Enhance Returns Experiences:

The “COVID Consumer” brings with it two new dynamics relating to product returns...

- Increased buying online will result in a greater volume of returns

- This new desire to spend less time in a physical retail location

A recent study (before COVID-19) on apparel retailers found the typical return rate for apparel purchases is 17%, however, this data did not separate physical and online retail.

The ability to streamline, simplify and enhance “returns experiences” is the retailer’s new loyalty strategy.

The data also proves there to be a correlation between great returns experiences and online conversion rates. This makes sense because simple and elegant returns experience de-risks the online purchase.

How many times has an in-store salesperson closed a sale by saying, “if you don’t like it you can always bring it back”?

Some examples of how retailers are creating amazing returns experiences…

“Return Window”:

Increase the “return window” which is the length of time a customer has to return an item. Sephora, Victoria Secret, and Gap have doubled the length of time customers have to return a product.

Improve the “Returns Story”:

Improve the “returns narrative” on the site…

If a customer has to fill out a form, show the form and explain what information needs to be filled out.

Document the returns process.

Provide estimated timelines as to when items will be returned, and money will be refunded.

Explain who pays for the postage.

Returns transparency:

When customers post a return back to a specific location, they are handing back a product without immediately receiving a refund. This creates anxiety.

To improve this, retailers need to activate triggered email notifications to update the customer on every step of the return, including when the money will be credited back.

#4. Supply local and be vocal:

As a result of the proven anxieties around supply chain along with the “COVID Consumer’s” gravitation to local products, retailers need to respond accordingly.

Promoting a product’s local origins will help: 11% of global consumers have changed to purchasing products manufactured in their own country while an additional 54% “mostly” bought local products.

Many international businesses have already invested “in-market” with local sourcing and manufacturing operations but very little of this is known to consumers. Be vocal and scream from the rooftops as to how the local industry is being supported.

Retailers who do not support the local supply chain need to rethink this approach. Consumers are now using “local credentials” as part of their criteria on who to engage with.

Even if sourcing products locally is impossible, being seen to be making effort in sourcing other materials locally helps. One example is sourcing recyclable packaging material locally.

#5. What and how to communicate:

What to communicate:

When looking specifically at the Australian consumer, 87% said they are happy to receive information from retailers.

Due to the high volume of information bombarding the “COVID Consumer”, it’s important to communicate what’s important to them in relation to how they want to engage with you.

The research summarized three communication themes….

- Promotion material

- Status of the business

- Content that helps the consumer evolve to their new way of life

Promotion Material:

As stated earlier, this is high on the priority list, and will be a method retailer can use to reignite engagement.

Status of the business:

Consumers are looking for the following types of questions to be answered about how a retailer is operating…

- Are stores open?

- Are you struggling to keep up with picking and packing online orders? If so how does that affect me?

- Are support teams available to engage with?

- Are there other options to pick up an order: click and collect? Is it safe?

Helpful Content:

This is content that assists in a consumer’s newly adopted way of life. For athletic brands it can be training tips, for kitchen retailers it can be “how to cook” and “recipe” content.

Nike recently opened up its paid subscription based “Nike Training Club” APP and made available all of its streaming workouts, training programs, and expert tips free to everyone.

Figure 10

Create helpful content around product:

For those retailers who do not have big content creation budgets, create and design content around products explaining how they help.

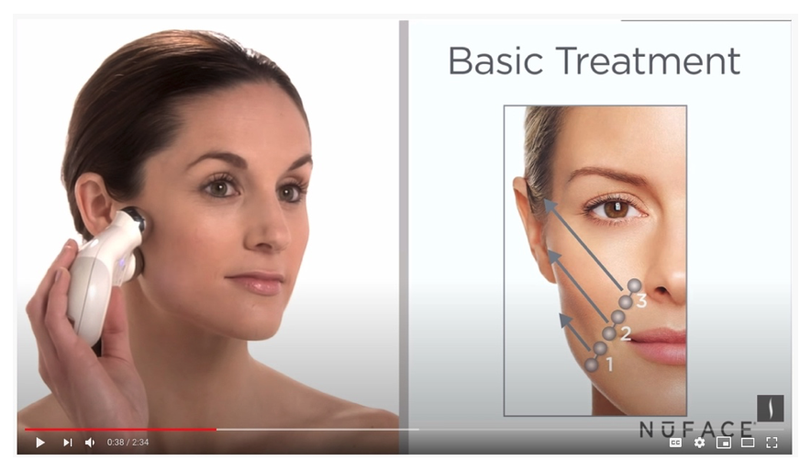

For example, the beauty brand NuFace, started creating facial toning content for its products because of the surge in demand for “at-home treatments” for skincare.

This content assists consumers in supporting their new desires to do more at home, and becomes powerful selling tools on product detail pages (see Figure 11).

Figure 11

How to communicate:

The most effective method to communicate is via email marketing. Since early March 2020, on average, consumers have been receiving 44% more emails than previous time periods.

Because consumers are seeking information from retailers, open rates have increased by 25% week on week. As of late April, 2020, open rates grew by 40%.

Data proves email subject titles where “Coronavirus” is used, has a spike in open rates but retailers must be careful of its use. Some retailers attempted to use this tactic to prompt opens and then presented sales campaign material instead of useful content on the pandemic.

This tactic resulted in low conversion rates and a negative view of the brand.

MIT Technology Review had this to say about this tactic…

“People don’t want marketing to make them feel anxious and fearful—the application of pressure harms brand integrity.”

Because a consumer’s inbox is being inundated, retailers need to consider the other alternatives to drive communications so as to stand out from the noise. While email marketing can be the foundation, the ideal method to get messages to consumers is via a “digital mix”.

Other proven forms of effective communications being used are….

- Social

- SMS

- Featuring content on the site

- When consumers email their questions, respond with answers but also introduce links to informative content

#6. Omnichannel:

The omnichannel retail strategy has heightened in its importance during COVID-19 as a result of two dynamics brought on by the new “COVID consumer”:

- The return to physical retail will be slow

- Consumers who do return to retail wish to spend less time in stores

Omnichannel becomes a significant contributor because…

- It will stimulate and prompt the return of consumers in store

- It will allow consumers to be better prepared when they venture into stores

The past successful tactic of running “in store events” will not be successful for some time.

Figure 12 (below) is summary of what consumers look for when there is intent to head to a physical retail location: product pricing and product inventory availability are the top two.

Figure 12

The two omnichannel activities seen to best align to these new needs is the presentation of inventory transparency and click and collect. This should form the foundation of every retailer’s omnichannel strategy.

Inventory Transparency:

Having accurate and intuitive “Check stock in store” experiences on product detail pages enables consumers to see if a product is available in a store the consumer selects. This is a proven foot traffic driver.

“Pre COVID” data shows 25% of consumers will not venture into a physical location unless they know a specific product of interest was in stock and available to view.

Click and Collect:

The offer of click and collect has steadily grown in popularity over the last few years with on average, 40% of online orders being fulfilled in this way (this grows beyond the 70% range during Christmas period).

More importantly, 85% of those recently surveyed, purchased extra items once in store to pick up their order.

Recently, the ability for retailers to offer a “contact-less” version of this pick-up service has been looked upon favourably, to reduce anxiety.

However, the evolution of click and collect should be looked at in other ways. Retailers must now consider how to keep this low contact option available and enable it to scale.

One example of achieving this is through the use of lockers at store locations.

Research shows the top four reasons consumers use click and collect are to…

- Save on Shipping Costs. Consumers expect this service to be free.

- Speed of Fulfillment. Consumers expect this service to be a faster method to acquire a product.

- Convenience. Consumers don’t want to waste energy looking for the click and collect counter.

- Assurance. Two of the biggest challenges with buying products online is getting the fit right for garments and making sure the product is what they wanted. The consumer uses click and collect so they can inspect the product at the store.

All four of these needs can be achieve through the use of lockers.

Walmart Pick Up Towers:

Walmart is in the process of installing an extra 900 “pick up towers” in stores, which will see 1,700 in total across its store network in the US. These lockers are designed in various sizes to allow for large items like TV’s to easily fit.

Figure 13

Since the acquisition of Wholefoods, Amazon has installed lockers in 76 locations which has been a pick up option for all Amazon products for consumers who reside in those regions.

For smaller retailers, this initiative can still be achieved through the ability to partner with Malls that offer these locker systems. Malls are constantly attempting to be seen as adding value to retailers: this becomes one such opportunity.

Stockland has partnered with Amazon to install “Amazon lockers” for self-service pick-ups across various mall locations in New South Wales and Victoria.

If malls open this up to retailers, once in place, these lockers can then also extend out to become a method to simplify returns (see improving returns experiences above). Before COVID-19 impacted retail, the consumer behaviour of buying online and returning that item into a physical store grew by 38% year on year. This behaviour is predicted to grow.

“Dark Stores”:

Instead of closing down underperforming sites, successful retailers are turning them into “dark stores”.

This type of store format is a retail outlet designed for the purpose of picking and dispatching online orders, ideally for customers within close proximity. The purpose of this store format is to increase capacity and scale for processing online orders.

However, if designed right, this can also become a valuable click and collect (and return) location.

Bed Bath & Beyond in the US has planned to transition 25% of its stores into regional fulfillment centers and Kmart Australia has permanently converted three of its locations to this store format.

While many retailers have temporarily activated “dark stores” during shutdown periods, such as Accent Group, this retail strategy is seen as the future.

Blake Morgan, author of “The Customer of the Future” is quoted in Forbes….

Even after the coronavirus has subsided and consumers try to return to some kind of normalcy, we’ll be faced with a new normal. Shoppers who have experienced delivery, curbside pickup and e-commerce will likely adopt at least some of those habits into their everyday lives. Many stores may still limit the number of customers inside at a time or instill social distancing measures. Dark stores help ease all of those transitions while still protecting customers and employees.

#7 Innovate:

Before discussing the value of embracing innovation, this term needs to be defined. The challenge in its definition is due to the fact that its perceived differently based on each business and its circumstance.

Things that influence the meaning of “innovating” will depend on business history, its own model, and culture and values.

To look beyond these nuances, and for the sake of this research, innovation for retailers is defined as…

The ability to create new and potentially valuable ideas in any retail activity.

Innovation is the process of transforming these ideas into a commercial reality.

“Innovation” is a fancy word for change that helps the customer.

As a result of the impacts brought on by COVID-19, businesses are seen to be innovating but not in the way most would think, it’s not “sexy”.

An “innovation” analysis was done on 300 organisations who turnover more than $100 million AUD annually and found the following as a direct result of the COVID-19 outbreak..

- 47% of businesses observed product or service innovations

- 49% have observed innovation in marketing messaging and branding

- 43% have observed innovation in customer communications

- 60% have observed innovation in the use of new processes

All these businesses plan to continue these new practices post-outbreak. Of the 300 researched, 23% planned an increase in spending on technology and infrastructure to embed these new changes into processes and systems.

Innovation – New ways to engage:

The other trend occurring within retail is the new use of existing technology that previously had proven to be ineffective.

Two examples of this and how it is currently impacting retail…

- Live one-on-one video

- Augmented reality

These tools did not work previously for a few reasons…

- Inadequate investment

- “Set and forget” mentality

- The “COVID Consumer’s” increased need for remote engagement options

The “set and forget” issue is important to note. Many retailers would activate a new technology because they were sold “the dream” of how it would improve engagement.

There was no consideration of the work required to elegantly integrate this technology into the broader infrastructure and more importantly, allocate resource to take consumers through this new way to engage.

Those winning, know they must invest, and guide their customers through new engagement options.

John Lewis - Live Video Example:

As a result of COVID -19, John Lewis launched an online engagement hub dedicated to a variety of “virtual services”, with the purpose of leveraging the instore expertise of their employees and make them more accessible in the digital context.

John Lewis is calling this service, “Your Partners Through It All”.

Consumers can book one-to-one video appointments with employees across different categories: how to set up a nursery (see Figure 14 below), interior design, and personal styling.

Figure 14

Kendra Scott - Augmented Reality example:

The US jewelry brand, Kendra Scott is using “virtual try-on’s” as an assisted method to enable online shopping.

Customers can place jewelry pieces on themselves through an augmented reality experience embedded in their site.

Figure 16

The retail staff are taking consumers through this technology and providing tips on how to use it to bolster engagement and ensuring positive experiences while it’s in use.

#8 Order management and fulfillment:

The vulnerability of supply chains has resulted in the “COVID Consumer” gravitating to retailers who can adhere to “reliable delivery” promises.

A retailer’s ambition to dramatically grow online revenue and transaction volumes is now being experienced by many. However, due to a lack of preparedness, many retailers are succumbing to operational chaos in the order management and fulfillment function.

For the sake of clarity, “order management and fulfillment” is defined as every business activity required to take a purchased product and get it into the hands of the customer.

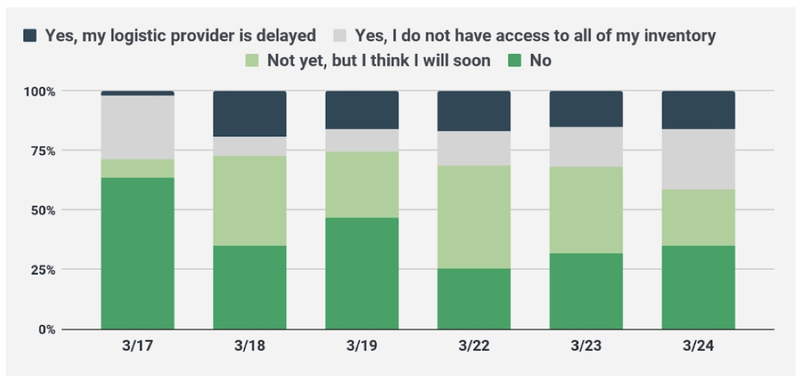

Figure 17 (below) is a business survey completed in late March 2020 where the question was asked, “Are you experiencing issues with your order management/fulfillment function?”

Over 66% of respondents stated they either had issues now (April/May 2020) or predict issues to be occurring soon.

Figure 17

“Labor intensive” vs “Labor reliant”:

The reason for this is, the fulfillment function is not “labor-intensive” it’s “labor-reliant”.

Executing systems and processes to fulfill an online order requires….

- Products to be taken from inwards and put on the shelf

- The picking of a confirmed order

- The packing and preparation for shipment of a confirmed order

There are many “hands” touching a single order. When fulfillment systems are not designed for scale, more “hands” touch the same order, increasing operational costs.

Businesses design operational costs around when things go according to plan, very few have a clear assessment of the increase in costs when operations do not run smoothly.

How can retailers scale a labor-reliant function in a COVID world?

All it takes is one warehouse employee to test positive for COVID-19 to put this entire business function at risk. Retailers need to design this part of the business for a “COVID World” which will permanently increase operational costs to the business.

Designing this function for scale is strategically important for two reasons…

- Being prepared for operations in a “COVID World” will increase costs

- Online sales will continue to grow

Without scale, profits will steadily degrade.

There are five primary methods to prepare the order management and fulfillment function to effectively operate and scale in a “COVID world”.

#1. Order Management and Fulfillment Software:

Introducing the right software will deliver a high level of logic and intelligence that will actively control and scale this labor-reliant function.

Some characteristics of what this software needs to do for a business…

- Capture and reduce human error (46% of fulfillment errors are from employees)

- Enhance business reporting – transparency

- Improve inventory accuracy

- Enable the capability of a high standard of email notification messaging to be sent to the customer

- Can rapidly send the order information to the right picking and packing site based on unique business rules and logic

- Be able to accurately and rapidly send and receive information from one business system to another

- Tight connectivity with eCommerce technology

Point 7 cannot be understated. The robust integration this software must have with eCommerce technology enables rapid and accurate information to move from one system to another.

It’s important to remember this connection is “two-way”. Not only is the eCommerce technology passing information to the order management system, but the order management system should be passing order updates for customers to view in their own my-account area.

This function alone contributes to scale due to the better information customers have access to in the context of the progress of their order.

#2. “COVID-Care plan” for warehouse employees:

A senior analyst from Gartner, highlighted the main challenges fulfillment operations will experience are the practices required in keeping employees safe while working: keeping warehouses and factories operating, and keeping products flowing.

Amazon has come forward stating they are introducing COVID related safety procedures and testing stations in all US distribution centers in the efforts to construct what they are calling a “COVID-free supply chain” (as mentioned earlier).

#3. Partner with specialist third party logistics:

The partnerships with 3PL’s has grown in popularity as a result of COVID-19. The intricacies behind how this could work will differ for each retailer, but this partnership does have potential benefits for those retailers who feel exposed…

- They take on all new procedure and system changes to prepare for the “COVID World”.

- They take on the associated capital costs (which may be passed on, but this can be negotiated).

- All employee management and support are controlled by the 3PL.

#4. Enhance transparency to customers:

It has been openly documented the large-scale issues that have arisen with last mile courier companies around the world. To put this in perspective, both Fed Ex and UPS have announced the suspension of their own service guarantees.

Suspension of Service Guarantee

Effective March 26, 2020 and until further notice, we have suspended the UPS Service Guarantee for all shipments from any origin to any destination.

As the effects of the Coronavirus impact our infrastructure, we will continue to seek guidance from local, state, and national government entities to ensure that we fully align with their regulations.

How can retailers respond by ensuring a great delivery experience to their customers?

There are two answers to this…

- Promote click and collect to reduce the reliance on home delivery

- Improve the notification experiences to keep customers informed

With the right order management system in place, there can be established “triggers” which would send elegant messaging notifying a customer with an update throughout the home delivery process.

#5. Dark Stores and Click and Collect:

The omnichannel section talks to the value and importance of Dark stores and click and collect. The impacts these initiatives have on contributing to scaling the fulfillment function is another benefit.

Conclusion:

Those retailers who pretend to be “customer first” are being exposed at present as well as those who have used their physical stores as a crutch to compensate for poor online experiences.

The “COVID Consumer’s” tolerance for poor online experiences has now become much lower than before because of their increased dependency on this digital method of engagement.

All the businesses seen to be winning have one common denominator: it’s all about the creation of amazing end-to-end online experiences.

This need to plan and construct amazing experience is known as “experience design”:

A process which creates an intuitive journey that acknowledges each micro-step a consumer takes must be met with relevancy and add value to his/her online experience.

The “experience design” comes from insights gained from the customer, and is then supported by processes, resource, technology, and business systems all working harmoniously together

Though every business is still in crisis mode, these are exciting times.

Every retailer is now on a level playing field, everyone must change and adapt. It’s now literally a race to uncover the needs and the motivations of the “COVID Consumer”, define how they want to engage, and to iteratively evolve as rapidly as possible.

It is the hopes this research has provided you, the retailer, a momentous step ahead of your competitors in the race to meet the needs of your new “COVID Consumer”.

This article was as tagged as Customer Service , Digital Strategy , eCommerce Consulting , UX Design